Fast Facts

The Ennoconn Kontron takeover bid, launched on June 11, 2026, marks a massive €1.47 billion mandatory acquisition event that permanently alters the European hardware landscape. Under the terms of the official regulatory offer, Ennoconn—a core Foxconn subsidiary—is acquiring Austria’s Kontron at €23.50 per share to lock down the embedded computing and edge AI hardware modules powering industrial IoT ecosystems across Europe.

📊 By the Numbers

- €1.47B — Ennoconn’s mandatory takeover offer valuation for Kontron, at €23.50 per share (Reuters / TradingView, June 11, 2026)

- 4.2% — Premium above Kontron’s closing price — barely above market, signalling Ennoconn’s confidence it doesn’t need to pay up (Finimize, June 11, 2026)

- €363.7M — Kontron Q1 2026 revenue, against a 2026 adjusted EBITDA target of €225 million (Kontron IR, May 2026)

- NT$10B+ — Ennoconn’s physical AI business revenue target for 2026 (US$318.93M), deepening its IIoT platform ambition (Digitimes, June 1, 2026)

- 7,000 — Kontron employees across embedded computing, IoT, and edge AI divisions globally — 500 earmarked for cuts under its turnaround plan

The Ennoconn Kontron takeover bid announced June 11, 2026 is being reported as a €1.47 billion M&A event. The financial mechanics are accurate. The strategic framing is incomplete. What Ennoconn — a subsidiary of Foxconn Technology Group — is acquiring isn’t just an Austrian technology company. It is the embedded computing and edge AI hardware that underpins industrial IoT deployments across European manufacturing, railway communications, smart energy, and factory automation.

Whoever controls that hardware layer controls where industrial data is processed, how fast edge decisions are made, and what upgrade path every Kontron customer faces for the next decade. That is not a secondary implication of this deal. It is the deal.

Why the Ennoconn Kontron Takeover Targets the Strategic IIoT Edge Layer

Kontron’s product portfolio — single board computers, embedded modules, industrial PCs, edge AI systems — sits at the precise point in the IIoT architecture where sensor data is first processed before it reaches the cloud or the analytics layer. Industrial IoT architecture frameworks consistently identify the edge computing layer as the highest-leverage point for latency reduction, cost control, and data sovereignty. It is also the layer most exposed to supply chain dependency.

Kontron’s 2024 revenue of €1.685 billion, its presence in railway systems, factory automation, and smart energy infrastructure, and its 7,000-person global workforce represent an embedded position in European industrial infrastructure that cannot be replicated quickly by a competitor. IIoT ROI models in 2026 are increasingly built around edge computing capability — which makes ownership of the hardware platform an operational and commercial dependency that Ennoconn now controls.

The 4.2% Premium Tells You Everything About the Power Balance

A 4.2% premium in a takeover offer is not a generous bid. It is a signal. According to Finimize’s June 11, 2026 analysis, “this isn’t a sudden takeover attempt so much as a regulatory checkpoint” — Kontron’s board had already authorised Ennoconn to cross the 30% ownership threshold, making the mandatory bid a formality rather than a contest. Ennoconn was already the largest shareholder. The bid simply converts de facto control into legal ownership.

For Kontron’s industrial customers, the threshold crossing matters more than the offer price. Kontron has simultaneously paused its share buyback and is executing a turnaround plan that includes cutting 500 jobs and targeting €225 million in adjusted EBITDA for 2026. That restructuring is now happening under the oversight of an acquirer whose physical AI revenue target for 2026 exceeds NT$10 billion — and whose parent company, Foxconn, has deep integration ties to a concentrated customer base that includes Apple. The connectivity infrastructure reshaping Industry 4.0 is increasingly concentrated in fewer hands — and this deal accelerates that concentration.

“The price is telling: €23.50 is only a 4.2% premium to Wednesday’s close — barely above where the market already pegged Kontron. This isn’t a contest. It’s a consolidation.”

— Finimize Analysis, June 11, 2026

Procurement Check-Sheets Following the Ennoconn Kontron Takeover

For the manufacturers, utilities, and infrastructure operators who rely on Kontron embedded systems, the ownership change raises three operational questions that procurement teams should be asking before the deal closes. First: do your existing Kontron supply agreements contain change-of-control clauses, and if so, what do they trigger? Second: does your IIoT architecture have hardware-layer dependency on Kontron-specific embedded modules that would create migration costs if pricing or supply terms change post-acquisition? Third: what is your contingency supplier for edge computing hardware if Kontron’s product roadmap shifts under new ownership?

These aren’t speculative concerns. 5G RedCap deployments in 2026 depend on edge hardware stability over multi-year rollout cycles. A change in Kontron’s product strategy — driven by Ennoconn’s physical AI priorities rather than European industrial IoT requirements — could create compatibility gaps in deployments that were scoped against Kontron’s current roadmap.

⚠ Fiction — Illustrative Scenario

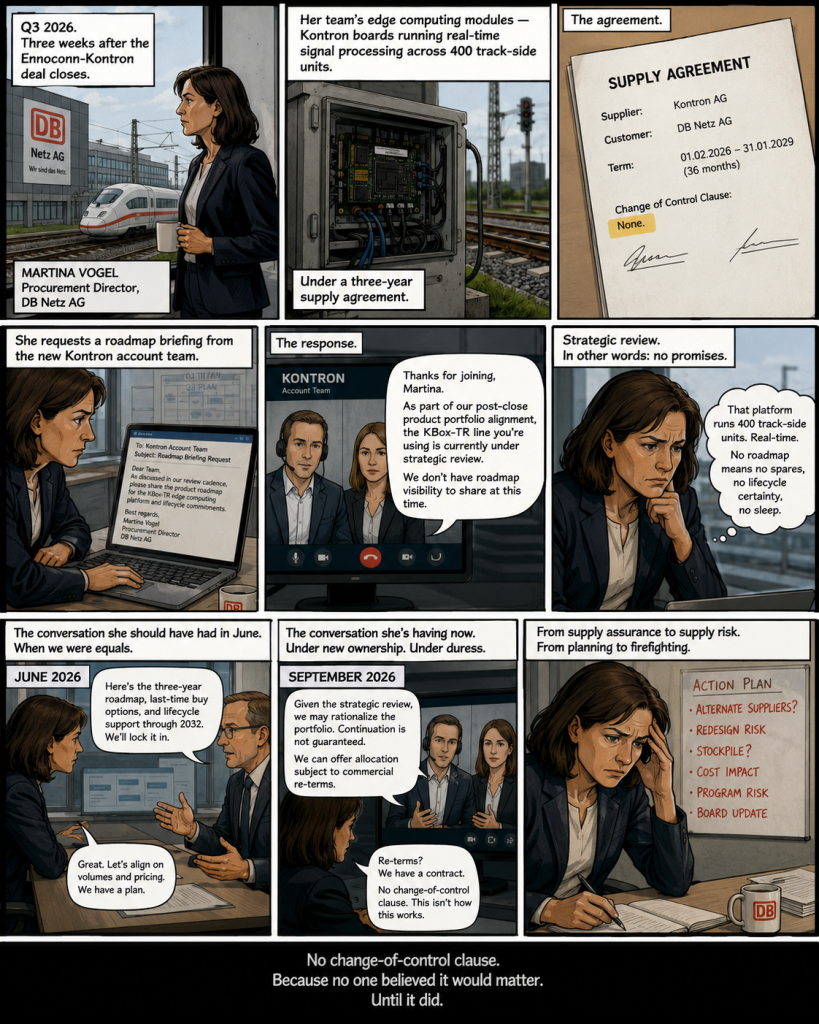

A procurement director at a German rail infrastructure operator reviews her hardware supply agreements in Q3 2026, three weeks after the Ennoconn-Kontron deal closes. Her team’s edge computing modules — Kontron boards running real-time signal processing across 400 track-side units — are under a three-year supply agreement. The agreement contains no change-of-control clause. When she requests a roadmap briefing from the new Kontron account team, the product line she specified is under “strategic review.” The conversation she should have had in June is now a renegotiation under duress.

Global Hardware Disruption via the Ennoconn Kontron Takeover

For industrial operators in Nigeria, Ghana, and Southeast Asia who have specified Kontron hardware in IIoT rollouts or procurement pipelines, this acquisition adds a supply chain concentration risk that wasn’t visible six months ago. Kontron’s distribution across emerging markets runs primarily through regional system integrators who source from European inventory. Ownership concentration at Foxconn levels creates the same single-point dependency risk that the audit-driven IIoT adoption crisis has consistently identified as a deployment vulnerability.

The IIoT chipsets market is projected to reach $97.8 billion by 2030 (Research and Markets, 2024). Ennoconn’s move to consolidate one of its most important edge computing suppliers is a deliberate positioning play for that growth — but the value it captures comes directly from the dependency it creates in the installed base it now controls.

💡 CreedTec Analyst’s Note

Daniel Ikechukwu — Strategic Impact

The Ennoconn-Kontron deal is the clearest signal yet that the IIoT edge computing layer is being treated as strategic infrastructure worth acquiring at scale — not just supplying. Foxconn, through Ennoconn, now controls embedded computing hardware that European industrial operations depend on daily. For Kontron customers, the risk isn’t immediate disruption. It’s a slow realignment of product roadmaps, pricing structures, and supply priorities toward Ennoconn’s physical AI agenda — which may or may not align with European industrial IoT requirements over the next three to five years.

- Stop: Treating this as a standard M&A event with no operational implications. If your IIoT deployment uses Kontron hardware, this deal changes your supplier’s strategic ownership. Audit your change-of-control exposure before Q4 2026.

- Start: Mapping hardware-layer dependency in your IIoT architecture. Identify any Kontron-specific embedded systems without qualified alternative suppliers — those are your supply chain risk nodes.

- Watch: Kontron’s product roadmap announcements under new ownership, particularly for edge AI modules and embedded computing lines. Any discontinuation or repricing of current product lines will be the first visible indicator of strategic realignment.

ROI Outlook: For industrial operators with current Kontron hardware, near-term ROI is unaffected. The risk window opens at the next procurement cycle: 12–24 months from deal close. Facilities that map their hardware dependency and qualify alternative suppliers now will have negotiating leverage. Those that don’t will be renegotiating under new ownership terms without options.

FAQ: Ennoconn Kontron Takeover & Europe’s IIoT Infrastructure

What triggered the mandatory Ennoconn Kontron takeover bid in 2026?

Under Austrian takeover laws, when an investment group or parent entity surpasses a 30% baseline shareholding stake in a publicly traded firm, they must launch a formal corporate offer. Ennoconn crossing this legal regulatory checkpoint triggered the mandatory €1.47 billion valuation bid at €23.50 per share.

How does this hardware consolidation impact industrial edge computing architectures?

Because Kontron manufactures the embedded computing, single-board configurations, and edge AI processing modules powering European rail, grid utilities, and automated lines, this ownership consolidation allows Foxconn’s subsidiary to hold deep strategic control over localized data sovereignty and multi-year product development roadmaps.

What does Ennoconn’s takeover mean for current Kontron customers?

In the short term, operations are unaffected — supply continuity and existing contracts remain in force. The medium-term risk is product roadmap realignment. Ennoconn’s physical AI agenda may redirect Kontron’s development priorities. Customers should review supply agreements for change-of-control clauses, qualify alternative edge computing suppliers, and request roadmap briefings from Kontron before the deal formally closes.

IIoT supply chain intelligence, hardware dependency analysis, and procurement strategy — built for operators who need the full risk picture before signing.