Last Updated 2026

Fast Facts

China humanoid robot mass production in 2026 has delivered what Tesla has not: commercially available units at scale. Unitree sold 5,500 humanoid robots in 2025. AgiBot crossed 5,000 units off the line. UBTech targets 5,000 more in 2026. Tesla has yet to sell a single Optimus commercially. This isn’t a technology race anymore. It’s a supply chain race — and China ran it first.

📊 By the Numbers

- 13,000–18,000 — Humanoid robots sold globally in 2025 (Omdia and IDC, via Rest of World, February 2026)

- 5,500 — Unitree humanoid robot sales in 2025 — world’s top seller by volume (Rest of World, February 2026)

- 5,000 — UBTech humanoid robot production target for 2026, doubling to 10,000 in 2027 (CNBC, December 2025)

- $38B → $5T — Global humanoid robot market by 2035 and 2050 respectively, with China projected at 60%+ share (Morgan Stanley, via Rest of World)

- 20–30% — Annual production cost reduction UBTech projects, enabled by supply chain density and state subsidies (IDN Financials, December 2025)

The China humanoid robot mass production race in 2026 settled a question that was still theoretical in 2024: who reaches commercial scale first? The answer arrived in February 2026, when Rest of World published Unitree’s first-ever sales disclosure — 5,500 humanoid robots sold in 2025, making it the world’s top-selling humanoid robot company by volume. Tesla, by comparison, had deployed fewer than 50 Optimus Gen 2 units internally and had not sold a single robot commercially.

The technology comparison between Optimus and its Chinese competitors is genuinely close. The supply chain comparison is not. And supply chain is what determines who builds the market.

China Ran the EV Playbook. Now It’s Running It Again.

The pattern is recognisable to anyone who tracked China’s electric vehicle ascent. State-backed production targets. Aggressive cost reduction through domestic supply chain integration. Rapid volume scaling before Western competitors reach commercial availability. Then price competition that compresses margins industrywide.

According to IDN Financials citing CNBC, UBTech projects production cost reductions of 20–30% annually, “supported by a strong supply chain and local government subsidies.” China has more than 150 humanoid robot companies actively developing and deploying hardware. That density of competition — all drawing from overlapping supplier networks — drives component costs down faster than any single company’s internal roadmap can achieve. The humanoid robot labor model is already shifting — and the company that reaches price parity with human shift costs first captures the market.

Tesla’s Real Advantage Is Not the Robot. It’s the Training Data.

Tesla’s genuine competitive moat in humanoid robotics is not its hardware — Chinese manufacturers are closing that gap at pace. It is the years of real-world autonomous driving data from millions of vehicles that feeds Optimus’s AI training. No Chinese competitor has an equivalent corpus of real-world embodied AI experience at that scale.

That advantage matters for long-term AI capability. It matters less for near-term commercial deployment. The ROI case for humanoid robots in 2026 is built on repetitive industrial tasks — package handling, assembly line support, inspection — where task completion rate and unit cost matter more than general intelligence. A robot that costs 40% less and completes the target task at 85% accuracy competes effectively against a robot that costs more and achieves 92%. The procurement decision isn’t purely technical.

“China is currently leading while the United States is still in the early stages of commercialising humanoid robots.”

— Andreas Brauchle, Partner at Horváth, via IDN Financials, December 2025

The Production Numbers That Reframe the Entire Narrative

AgiBot’s 5,000th humanoid robot milestone, Unitree’s 5,500 commercial sales, and UBTech’s 5,000-unit 2026 production target collectively represent a market that has moved from demonstration to deployment. According to Rest of World’s February 2026 analysis, between 13,000 and 18,000 humanoid robots were sold globally in 2025 — the majority of which shipped from Chinese manufacturers.

Tesla’s GigaShanghai president Allan Wang Ho acknowledged the production dynamic directly in April 2026, describing the plant as a potential “golden key” to robot mass production — an admission that China’s manufacturing infrastructure is Tesla’s most plausible path to scale, not a competitor to route around. The Robot-as-a-Service model emerging from deals like Agility Robotics and Toyota may offer Western manufacturers a deployment path that sidesteps the unit cost comparison — but only if the per-task economics hold against Chinese pricing.

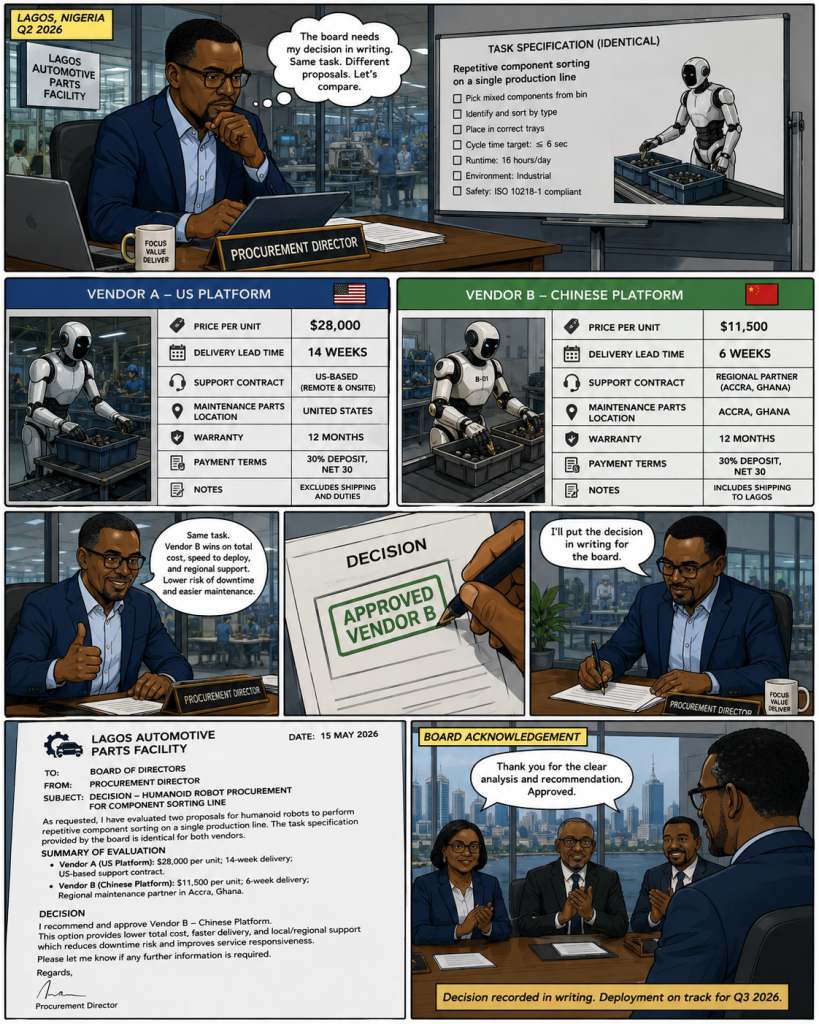

⚠ Fiction — Illustrative Scenario

A procurement director at a Lagos automotive parts facility reviews two humanoid robot proposals in Q2 2026. Vendor A — a US platform — quotes $28,000 per unit, with a 14-week delivery lead time and a US-based support contract. Vendor B — a Chinese platform — quotes $11,500 per unit, 6-week delivery, and a regional maintenance partner in Accra. The task specification is identical: repetitive component sorting on a single production line. The procurement director approves Vendor B. The board had asked for the decision in writing.

Emerging Markets Will Decide Who Wins the Second Wave

The first wave of humanoid robot deployment is happening in automotive factories in China, the US, and South Korea. The second wave — facilities in Nigeria, Ghana, Southeast Asia, and Latin America where labor cost arbitrage is narrowing and operational scale is growing — will be won by whoever reaches those markets with a commercially viable unit cost first.

China’s 20–30% annual cost reduction trajectory puts humanoid robots within procurement reach of mid-size emerging market industrial facilities by 2028–2029. Humanoid robots are already entering small-town factories in China’s interior — proving the deployment model works outside tier-one industrial clusters. Hyundai’s Atlas factory deployment demonstrates that Western platforms can also reach operational readiness — but the cost curve is running in one direction, and it is running faster on the Chinese side.

💡 CreedTec Analyst’s Note

Daniel Ikechukwu — Strategic Impact

The humanoid robot race in 2026 is not close in the dimension that matters most for near-term market share: commercial availability at deployable cost. China has it. Tesla doesn’t yet. The long-term AI capability advantage Tesla holds through its driving data corpus is real — but it plays out over years, not quarters. For industrial operators making procurement decisions today, the choice is between a commercially available Chinese platform with declining unit costs and a Western platform that remains in internal testing. That asymmetry will shape the installed base that all subsequent competition builds on.

- Stop: Framing the humanoid robot competition as a technology race. It is a deployment race. The company with the most installed units builds the most training data. The company with the most training data improves fastest. Unit count is the leading indicator.

- Start: Modelling total cost of ownership over 36 months for humanoid robot procurement — including unit price, maintenance contract geography, support response time, and retraining cost. Chinese platforms win on unit price; the comparison shifts significantly on support infrastructure.

- Watch: Tesla’s GigaShanghai production signal. If Optimus manufacturing moves to China, the unit cost gap narrows dramatically — and the competitive dynamic changes from “China vs Tesla” to “Chinese supply chain powering both.”

ROI Outlook: For facilities in emerging markets evaluating humanoid robot procurement in 2026, Chinese platforms offer the most accessible entry point on unit cost. The 20–30% annual cost reduction trajectory makes a 2027 purchase materially cheaper than a 2026 purchase — giving procurement teams a defensible case for a structured pilot now and a volume commitment in 18 months, when the price and reliability data both exist.

Frequently Asked Questions

Can you actually buy a Chinese humanoid robot commercially in 2026?

Yes. Unitree, AgiBot, and UBTech all have commercially available humanoid robots with documented sales. Unitree sold 5,500 units in 2025. AgiBot crossed its 5,000th production unit. These are not concept products — they are shipping hardware with active industrial deployments in automotive and logistics settings.

Should emerging market facilities buy Chinese humanoid robots over Western alternatives?

The unit cost case currently favours Chinese platforms significantly — potentially 50–60% lower than Western equivalents at comparable task specifications. The procurement risk is in support infrastructure: most Chinese vendors’ regional maintenance networks are thinner outside East and Southeast Asia. Evaluate total cost of ownership including support response time and retraining costs, not unit price alone.

What does Tesla’s Optimus timeline actually look like in 2026?

As of mid-2026, Tesla has deployed fewer than 50 Gen 2 Optimus units internally and has not made commercial sales. Mass production is planned but not yet delivered. Tesla China’s president identified GigaShanghai as a potential production facility — suggesting the unit cost and manufacturing scale problem may be addressed through China’s supply chain infrastructure rather than US-based production alone.

Humanoid robot market intelligence, procurement strategy, and deployment economics — built for operators who need the real competitive picture before they sign.