Fast Facts

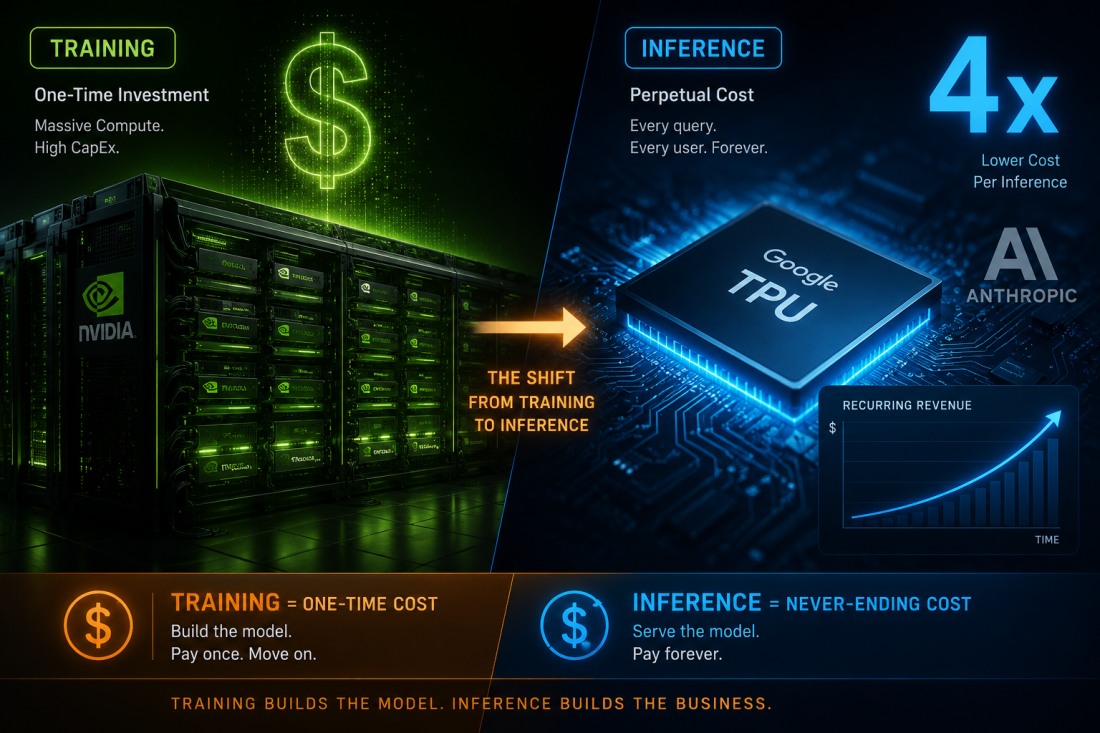

Google’s TPU push is chasing inference money, not Nvidia’s crown. Google is now selling TPUs directly to outside customers, with Anthropic alone committing to over a million TPUv7 chips. The real target isn’t Nvidia’s training-chip dominance — it’s inference, the ongoing cost of running AI models, which is quietly bankrupting the industry’s biggest names. OpenAI spent $1.35 for every $1 of revenue in 2025, driven mostly by serving requests, not training them.

- 1M+ TPUv7 “Ironwood” chips — Anthropic’s committed order from Google

- $42B — Google Cloud’s reported backlog growth tied to TPU rentals

- $1.35 spent per $1 earned — OpenAI’s 2025 economics, on $3.7B revenue and an estimated $5B loss

- 60–70% — share of hyperscaler AI compute now going to inference, up from ~40% in 2024

- 4x — Google’s claimed cost-per-token advantage for TPUs over GPUs on LLM inference workloads

Training Was Never the Expensive Part

Every AI cost conversation used to center on training: the eye-watering price of building a frontier model. That framing missed the bigger bill. For every $1 billion spent training a model, organizations face an estimated $15–20 billion in inference costs over its production lifetime — the ongoing compute needed just to answer users’ requests. GPT-4’s training reportedly cost around $150 million; its cumulative inference costs had already reached $2.3 billion by end of 2024.

“I said, ‘OK, if we want to have this speech model that we roll out to 100 million users… that would require doubling the number of computers Google had. We need to build specialized hardware.'” — Jeff Dean, Chief Scientist, Google DeepMind

Why the TPU Pitch Is About Recurring Revenue

Training is a one-time capital event — expensive, but finite. Inference is perpetual: every user query is a fresh compute cost that recurs for as long as the product exists. Google’s TPU rentals have driven roughly $42 billion of Google Cloud’s backlog growth, largely from Anthropic’s multi-year commitment — not a chip sale, but a recurring utility contract, the same model that made cloud computing durable and high-margin.

The Number That Explains the Urgency

OpenAI’s own economics show why this problem needed solving now. The company generated $3.7 billion in revenue in 2025 while losing an estimated $5 billion, spending $1.35 for every dollar earned — losses driven overwhelmingly by serving inference requests at scale, not R&D or headcount. Every major AI lab is running some version of that math, which is exactly the pressure Google’s cheaper TPU pricing is designed to relieve.

⚠ Illustrative scenario (fictional): A mid-size AI startup builds a chatbot on rented GPU inference, only to find its cloud bill scaling faster than subscription revenue as usage grows. Migrating inference to lower-cost TPU capacity — the same shift Midjourney reportedly made, cutting monthly compute costs from roughly $2 million to $700,000 — would turn a widening loss into viable unit economics.

Global Implications: Whoever Owns Cheap Inference Owns the Next Decade

Nvidia still commands the overwhelming majority of the AI accelerator market, and its CUDA software ecosystem remains deeply entrenched. But as AI shifts from a training-dominated to an inference-dominated cost structure, the company that makes inference cheapest — not the one with the fastest training chip — captures the larger, more durable revenue pool. For operators anywhere evaluating AI infrastructure, including emerging markets where compute cost is already a large share of budget, the lesson is the same: price your AI strategy around inference at scale, not training at launch.

💡 CreedTec Analyst’s Note — Daniel Ikechukwu

Strategic Impact: The AI industry’s real profit pool is shifting from one-time training spend to perpetual inference cost — and that shift determines who wins the infrastructure race, not raw chip performance.

Stop: Evaluating AI infrastructure vendors primarily on training benchmark performance.

Start: Modeling your AI product’s inference cost at projected scale, not just at launch volume.

Watch: Whether Meta and other major Nvidia customers follow Anthropic’s lead into large-scale TPU commitments over the next year.

ROI Outlook: Favorable for buyers diversifying inference workloads across TPU and GPU capacity; risky for those locked into single-vendor GPU contracts as inference volume scales.

Your AI bill won’t explode at launch — it explodes at scale. Subscribe to CreedTec’s newsletter for the infrastructure economics AI vendors don’t lead with.

Further reading on CreedTec:

TeraWulf’s Anthropic Deal Proves Power Beats Chips · CoreWeave’s Revenue Backlog as an Infrastructure Asset Class · AI Semiconductor Revenue Passes $1 Trillion in 2026 · Strategic AI Infrastructure Investment · OpenAI’s Revenue Growth in 2025