Fast Facts

Vodafone and Nokia’s AWS IoT trial isn’t a connectivity upgrade — it’s a cloud middleware land grab worth $73 billion. Whoever owns that processing layer owns the enterprise IoT revenue. Here’s what procurement teams and plant operators need to understand before signing.

📊 By the Numbers

| Metric | Value | Source | Year |

|---|---|---|---|

| IoT connections managed globally | 155M | Vodafone IoT Barometer | 2024 |

| Projected IoT cloud platform market | $73.4B | MarketsandMarkets | 2030 projection |

| Global cloud infrastructure spend share | 31% | Amazon Web Services via Synergy Research Group | Q4 2025 |

| Network-as-a-service revenue growth | +18% YoY | Nokia Annual Report | 2025 |

The Vodafone Nokia AWS IoT trial is being covered as a connectivity milestone. It isn’t. Announced in early 2026, the partnership between Vodafone, Nokia, and Amazon Web Services to run IoT applications over cloud infrastructure is a calculated move in a $73 billion race — and the financial logic behind it tells a completely different story than the press releases do.

Vodafone already manages 155 million IoT connections. Its gap isn’t devices. It’s the cloud services layer sitting above those connections — where the real recurring revenue lives.

The Cloud Layer Is Where the Money Actually Is

Industrial IoT generates enormous volumes of data. But raw device data, sitting on-premise, earns nothing. The profitable position is the managed cloud middleware — the layer that aggregates, processes, routes, and monetizes that data stream. AWS provides compute backbone. Nokia delivers network-layer credibility. Together, they hand Vodafone an enterprise-grade cloud IoT stack it didn’t have to architect from zero.

According to Nokia’s 2025 Annual Report, network-as-a-service revenues climbed 18% year-over-year — proof that hardware vendors are themselves racing toward managed cloud positioning. Vodafone is following the same logic one level up the value chain.

What Enterprises Are Not Being Told About This Trial

Cloud-dependent IoT platforms generate switching costs that are rarely visible at the contract signing stage. Once your IoT architecture is integrated into a managed cloud layer — firmware updates, analytics dashboards, SIM provisioning — migration becomes operationally painful and commercially expensive.

The procurement word for this is lock-in. It is never announced as a feature. Connectivity-as-a-Service contracts have fundamentally restructured how this dependency is packaged: what looks like flexibility often contains multi-year data gravity that benefits the vendor, not the buyer.

“Network-as-a-service revenues grew 18% year-over-year.”

— Nokia Annual Report, 2025

Why Emerging Market Operators Face a Specific Risk

For plant managers and procurement teams across Nigeria, West Africa, and Southeast Asia, cloud-hosted IoT management adds a risk layer that goes beyond vendor dependency: currency exposure. AWS infrastructure is billed in dollars. Revenue is earned in naira, rupiah, or cedi. Exchange rate volatility is no longer a finance department problem — it becomes an operational continuity risk embedded in your IIoT ROI model.

This isn’t hypothetical. 5G RedCap deployments and new connectivity standards like KORE Kigen SGP.32 are creating genuine infrastructure alternatives. The question isn’t whether to adopt cloud-assisted IoT — it’s whether you negotiate contractual leverage before you become dependent on the vendor’s rate card.

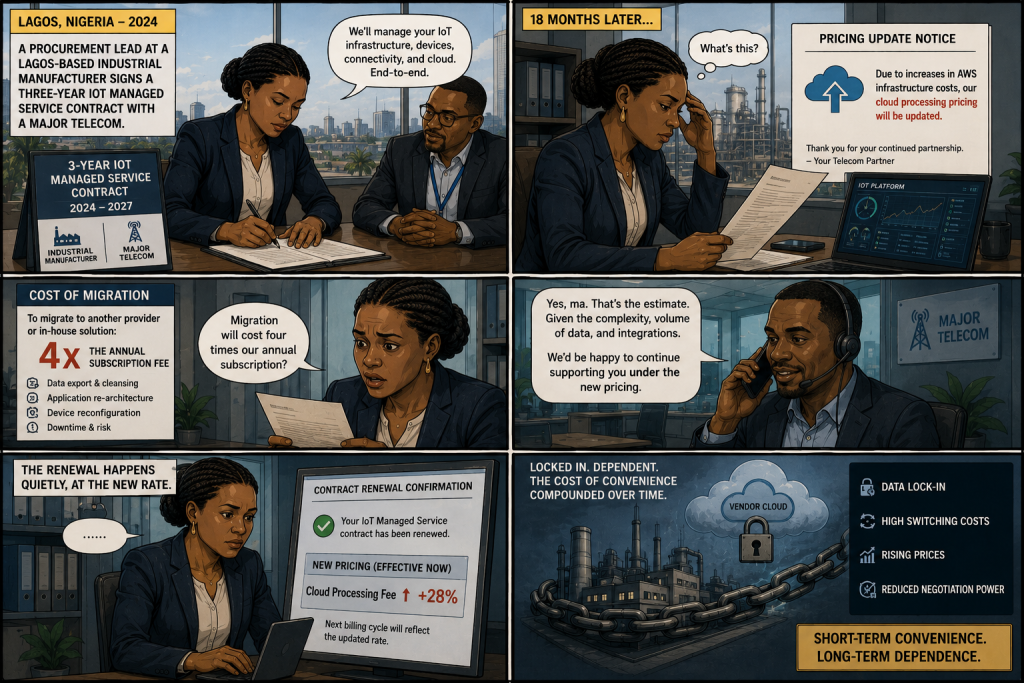

⚠ Fiction — Illustrative Scenario

A procurement lead at a Lagos-based industrial manufacturer signs a three-year IoT managed service contract with a major telecom in 2024. Eighteen months later, the vendor updates its cloud processing pricing, citing AWS infrastructure cost increases. Migration is estimated at four times the annual subscription fee. The renewal happens quietly, at the new rate.

💡 CreedTec Analyst’s Note

Daniel Ikechukwu — Strategic Impact

This trial accelerates the telco-to-cloud-platform pivot. Vodafone is no longer competing with other telcos on price — it is competing directly with Siemens, PTC, and AWS IoT Core for the enterprise platform contract. Nokia’s participation converts Vodafone’s pitch from “connectivity provider” to “full-stack industrial IoT partner.” That repositioning changes who sits at the procurement table and what gets signed.

- Stop: Signing long-term IoT managed service contracts without cloud-agnostic exit clauses.

- Start: Auditing your IoT data architecture for cloud dependency before your next renewal cycle.

- Watch: Whether Nokia extends this model into African and Asian markets through Vodafone’s existing 155M-connection footprint. If it does, emerging market operators will face this pricing structure within 18 months.

ROI Outlook: Short-term operational gains are real for enterprise early adopters. Medium-term, expect pricing pressure as switching costs solidify post-integration. Evaluate total cost of ownership over 36 months — not 12.

Industrial IoT strategy, financial logic, and market intelligence — no noise, no hype. Built for operators who think before they sign.

Join the Newsletter →