Fast Facts

The top robotics companies 2026 list should be sorted by balance sheet, not brand. Robotics companies worth watching in 2026 aren’t the ones with the biggest installed base — they’re the ones showing real growth and profit, while legacy leaders like FANUC and ABB post declining segment sales. For buyers signing multi-year contracts, financial trajectory predicts long-term support better than heritage does.

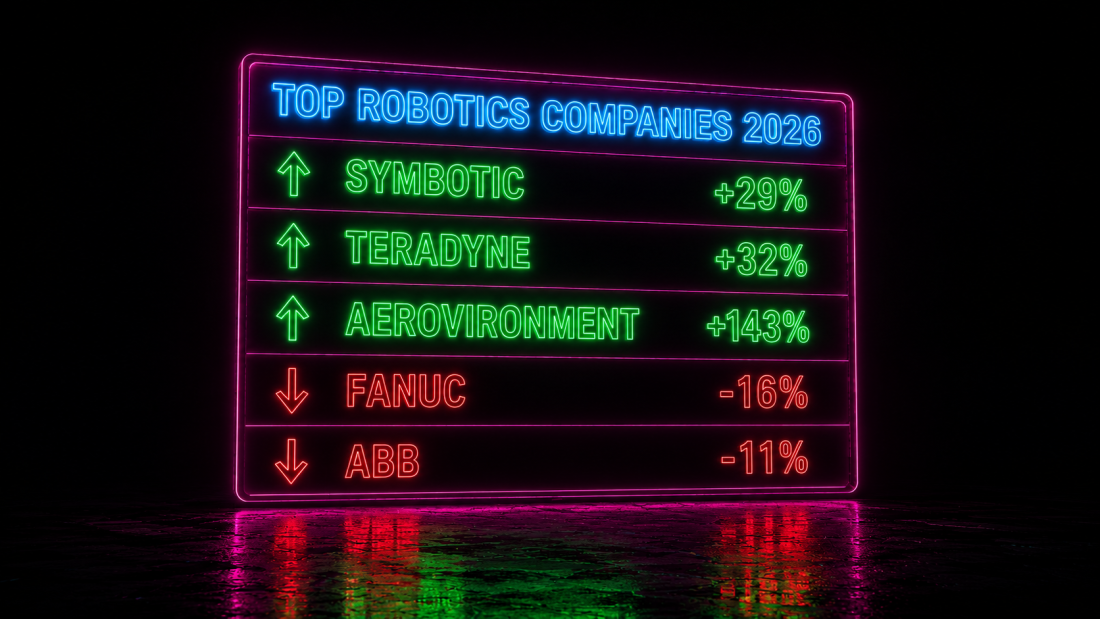

- $630M — Symbotic’s Q1 FY2026 revenue, up 29% YoY, net income $13M

- 143% — AeroVironment’s Q3 revenue growth YoY, to $408M; backlog $1.1B

- 32% — Teradyne’s robotics division (UR + MiR) Q1 revenue growth, to $91M

- -16.4% — FANUC’s robot sales decline in the first 9 months of FY2026

- $3.21B → down from $3.64B — ABB robotics division revenue, 2024 vs. 2023

- $89.86B — global robotics market size projected for 2026 (Statista)

The Split Nobody’s Pricing In

Robotics coverage still leans on installed-base bragging rights — FANUC’s 240,000 robots deployed, ABB’s 400,000-plus. Those numbers describe the past. They say nothing about whether a vendor’s current unit is growing or shrinking — the number that actually determines whether your support contract and software updates stay a priority five years from now.

Where the Growth Actually Sits

Teradyne’s robotics division — which owns Universal Robots and Mobile Industrial Robots — reported $91 million in Q1 revenue, up 32% year over year. Symbotic, which builds warehouse automation for Walmart and Albertsons, posted $630 million in Q1 FY2026 revenue, 29% growth, and $13 million in net income — a real profit, not just volume. AeroVironment’s tactical robotics revenue jumped 143% to $408 million, backed by a $1.1 billion order backlog.

“Attention has decisively pivoted toward companies producing verifiable outcomes.” — Parameter

Why Legacy Scale Now Looks Like a Liability

FANUC’s net sales still hit $4.1 billion through nine months of fiscal 2026, but robot sales specifically fell 16.4%. ABB’s robotics division brought in $3.21 billion in 2024, down from $3.64 billion in 2023 — enough of a decline that ABB is spinning the unit off as a separate public company, targeting a $3.5 billion valuation. Scale built a moat in the pre-AI robotics era; it now competes against buyers’ fear of being locked into a vendor whose core division is shrinking while its parent gets distracted by restructuring.

⚠ Illustrative scenario (fictional): A contract manufacturer picks a robot arm supplier on brand recognition alone, signing a five-year service agreement. Two years in, the vendor’s robotics division is spun off mid-restructuring, and support response times slip. Nobody checked whether the division’s revenue was growing before signing — only that the logo was familiar.

What This Means for Procurement Decisions

Rockwell Automation’s Q1 FY2026 sales reached $2.105 billion, up 12% YoY, with segment operating profit up 36% — recurring software revenue, not just hardware, is what’s compounding. The pattern holds: Symbotic, AeroVironment, Teradyne, and Rockwell are all growing on services, software, or backlog visibility, not installed-base counts.

Global Implications: The Capital Behind the Curve

Robotics startups pulled in over $2.26 billion in Q1 2026 funding, with more than 70% going to warehouse and industrial automation — capital chasing the same discipline signal buyers should watch. For operators in emerging markets weighing a robotics investment, the lesson travels directly: a five-year RaaS contract is only as reliable as the vendor’s current revenue trajectory, regardless of headquarters.

💡 CreedTec Analyst’s Note — Daniel Ikechukwu

Strategic Impact: Vendor financial health is becoming a sharper procurement filter than installed base or brand heritage as AI reshapes robotics competition.

Stop: Selecting robotics vendors primarily on name recognition or historical installed-base size.

Start: Pulling a vendor’s latest quarterly segment revenue and growth trend before signing multi-year service or RaaS contracts.

Watch: ABB’s robotics spin-off execution in 2026 as a signal of how legacy players restructure under AI-era pressure.

ROI Outlook: Favorable for buyers weighting financial trajectory in vendor selection; cautionary for those defaulting to legacy brands alone.

A shrinking robotics division doesn’t announce itself before your service contract does. Subscribe to CreedTec’s newsletter for the vendor signals procurement teams miss.